Meet Our Team

Our team of experts is dedicated to helping you. We proudly serve local neighbors in Orange County, Los Angeles, and across Southern California, while also assisting clients nationwide in every state except for Oregon.

Wherever you are, count on us to make things easy and ensure you are completely taken care of.

Nadia Ponce Simbron

PartnerLicensed Insurance Agent

LIC# 4431312

Calvin Vo

PartnerLicensed Insurance Agent | Tax Agent

LIC# 4438235

Haven Guide to Your Medicare Options

Turning 65 or retiring soon?

At Haven, we break down your choices to ensure your health coverage and financial planning work together seamlessly. Explore the four pillars of Medicare below.

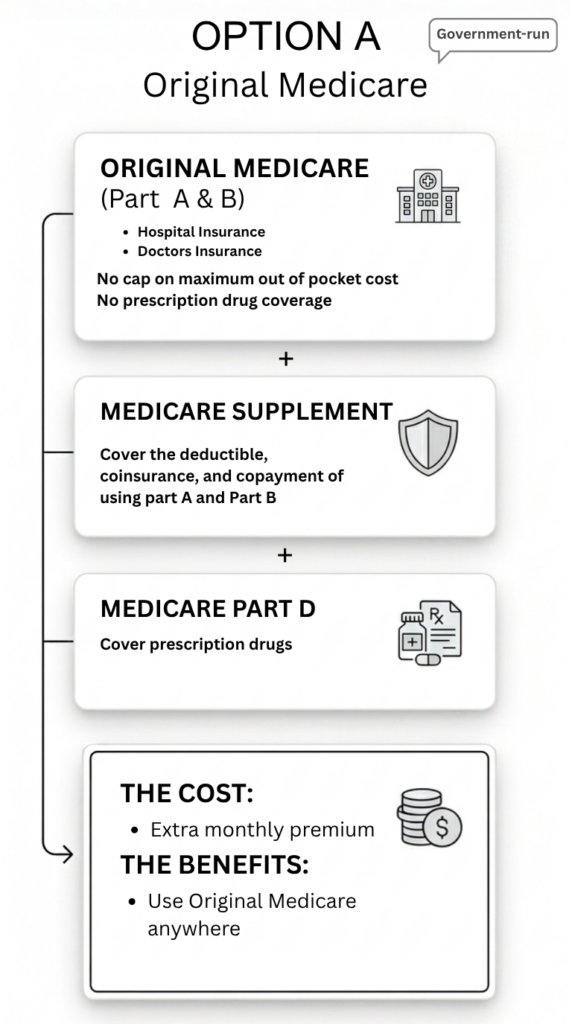

Part A (Required)

The first half of Original Medicare

Covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care. Part A is usually free to enroll for most people who have worked in the US for 10+ years.

To use Part A, it has require payments for deductibles and copays.

Part B (Required)

The second half of Original Medicare

Covers certain doctors’ services, outpatient care, medical supplies, and preventive services.

Part B has a monthly enrollment cost that often increase year to year and is dependent on your income.

You may face a permanent monthly penalty if you do not sign up for Part B when you first become eligible at age 65.

To use Part B, it requires a monthly premium, an annual deductible, and coinsurance payments.

Part D (Add-On)

Stand-alone plans that add critical prescription drug coverage

Original Medicare (Parts A and B) generally does not cover outpatient prescription drugs. Because of this, Part D is a necessary addition to your coverage to avoid paying the full retail price for medications.

You may owe a permanent late enrollment penalty if you go 63 days or more without creditable drug coverage after turning 65.

To use Part D, it requires a monthly premium, an annual deductible, and copayments or coinsurance for your medications.

Part C (Alternative)

An all-in-one alternative to Original Medicare

- Combines Part A, Part B, and usually Part D (MAPD) into one comprehensive plan.

- Often includes extra benefits like routine dental, vision, hearing, and fitness memberships.

- Usually have lower annual out-of-pocket maximum at the cost of staying in network.

Supplement (Add-On)

Medigap plans are private insurance policies that pay for the “gaps” in Original Medicare

- You pay a monthly fee to a private insurance company. Prices vary by plan type (e.g., Plan G, Plan N) and provider.

- Different plans cover different costs of using Medicare, such as your hospital deductibles, the coinsurance for medical services, and foreign travel emergency care.

- While there isn’t a government-mandated “tax” penalty like Part B or D, there is a significant risk: if you wait past your initial 6-month window at age 65 to join, insurance companies can charge you much higher premiums or deny you coverage entirely based on your health.

Part A: Deductible

$1,736 (Once every hospital stay for the year)

Part B: deductible

Part B: Co-Insurance for procedure

20% of total cost

Part B: Co-insurance for Doctor visits

20% of total cost

Frequently Asked Questions

We’re here to help: Navigating the dozens of available plans can be overwhelming. We can help you compare options to find the one that fits your specific prescriptions and budget; contact us today for free assistance.

Still have a question?

Opt-Out of Data Sharing

We value your privacy. Your information is used only to respond to your inquiry and is never shared with third parties without your explicit consent.

Specific Disclaimer for Medicare clients

By submitting this form, you agree to have a licensed insurance agent from Haven Tax & Insurance Agency contact you by phone or email to answer your questions or provide additional information about Medicare Advantage, Part D, or Medicare Supplement Insurance Plan and understand that I can opt-out at any time. You are not obliged to enroll. Calls are for marketing purposes. Cellular carrier charges may apply. Providing permission does not impact eligibility to enroll or the provision of services, and other consumers can change permission preference at any time by contacting the TPMO.

Haven Tax & Insurance Agency is a licensed insurance agency that works with Medicare enrollee to explain Medicare Advantage, Medicare Supplement, and Prescription Drug Plan options. Plans are available to anyone who has both Medicaid from the State and Medicare. Premiums, co-pays, co-insurance, and deductible may vary based on your Medicaid eligibility category and/or the level of “Extra Help” you receive. Please contact the plan for further details. Haven Tax & Insurance Agency is a licensed and certified representative of Medicare Advantage [ HMO, HMO SNP, PPO, PPO SNP and PFFS] organizations [ and stand-alone PDP prescription drug plans] that have Medicare contract. Haven Tax & Insurance Agency and Medicare supplement insurance plans are not connected with or endorsed by the U.S. government or the federal Medicare program. We do not offer every plan available in your area. Currently we represent [0-22] organizations which offer [0-685] products in your area. Please contact Medicare.gov, 1-800-MEDICARE, or your local State Health Insurance Program (SHIP) to get information on all of your options. We offer plans from a number of insurance companies.